The early stages of the COVID-19 pandemic produced an exodus of renters from gateway markets, prompting questions about their long-term future. While those questions remain unresolved, prospects for urban markets brightened in 2021 as apartment demand returned with the reopening of cities.

The gateway rebound comes amid record-setting demand nationally, as multifamily established a new annual high in absorption in only nine months. Through the first three quarters in 2021, 475,000 apartment units were absorbed in the U.S., already topping 2018’s single-year high of 370,000 recorded by Matrix. At least 100,000 units have been absorbed in each of the last four quarters, which is also a first.

The absorption numbers explain the industry’s recent extraordinary rent performance. Asking rents nationally were up 11.4 percent year-over-year through September, while the occupancy rate of stabilized properties rose 110 basis points year-over-year to 95.9 percent as of August, per Matrix data on 144 markets.

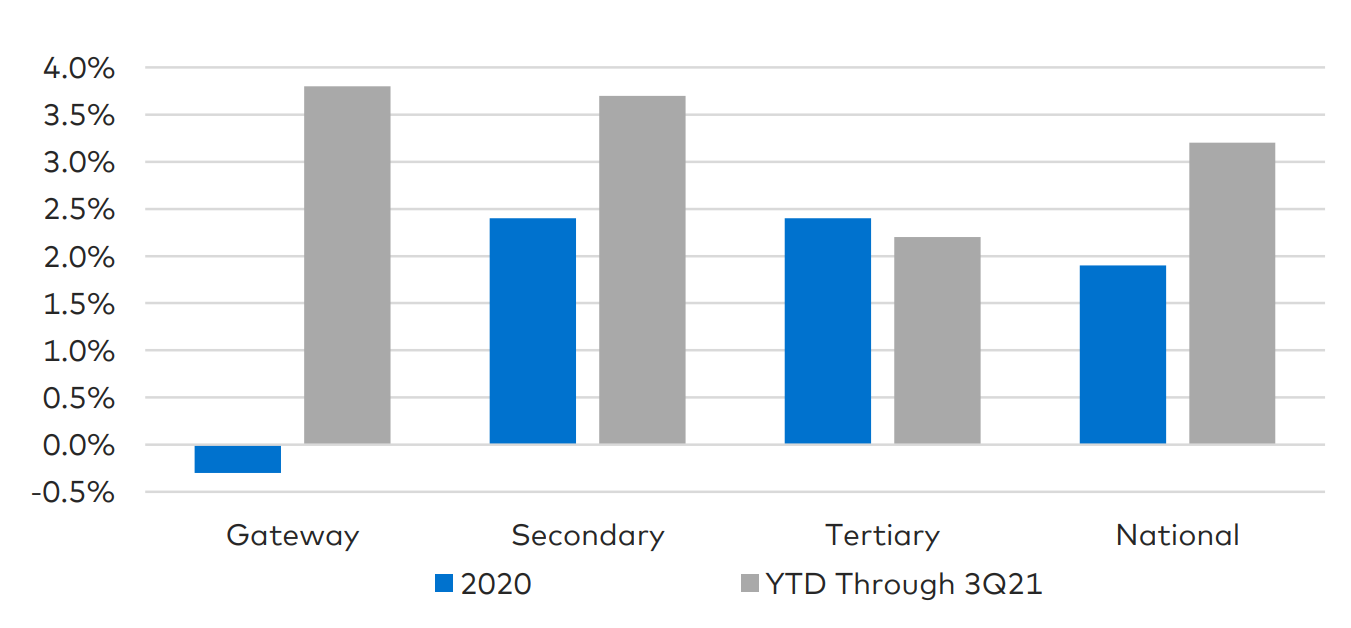

Absorption as % of Stock by Market Size

Robust multifamily absorption is driven by a confluence of factors, including robust economic growth, the decline in unemployment, pent-up demand coming out of the pandemic, and strong household savings. Plus, there remains a long-term shortage of housing supply, as new construction was stifled for several years coming out of the Great Recession, and single-family home prices have soared.

Arguably, the most notable part of the 2021 landscape is the rebound in gateway markets, which are on the verge of a “worst-to-first” turnaround. Gateway metros (which Yardi defines as New York City, Boston, Washington, D.C., Miami, Chicago, Los Angeles and San Francisco) combined posted negative (-7,000) absorption in 2020.

Through three quarters in 2021, gateway metros have absorbed some 108,000 units. As a percentage of stock, that amounts to 3.8%, which is the highest rate among metros ranked by market size. Secondary markets absorbed 3.7% of stock, while tertiary metros trailed at 2.2% of stock. In 2020, gateway metro absorption was -0.3%, compared to 1.9% for the entire U.S.

During the pandemic, gateway markets lost Millennial renters with children looking for housing with more space and/or better schools, renters who work remotely looking for lower-cost housing and those seeking a more suburban or rural lifestyle. Now units are being backfilled, largely by young workers seeking the experience of city life and downsizing retirees.

Regionally, the Southeast continues to attract the most renters, with 155,000 units absorbed year-to-date through the third quarter, or 3.7% of stock. Metros in the West (101,000, 3.3% of stock) and Southwest (98,000, 3.5% of stock) also are attracting a high number of households. The Northeast (60,000, 2.7% of stock) and Midwest (59,000, 2.5% of stock) trail in total absorption.

Multifamily has benefited from a confluence of factors to produce outstanding fundamental performance in 2021. Some of those factors, such as the stimulus-fueled GDP growth and pent-up demand after a year spent in quarantine, are not sustainable. Other factors that involve evolving social and demographic forces are likely to drive demand for years to come.

Read the full Matrix Bulletin-Absorption Paper-October 2021

Add Comment