Multi-family real estate investment trusts (REITs) second quarter results revealed a marked improvement in new lease pricing. Whether the portfolio is focused on coastal urban centers or suburban Sunbelt markets, second quarter reported results were a notable improvement over Q1 2021 and Q4 2020 new lease growth rates.

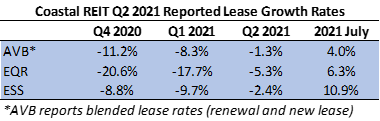

Coastal gateway markets have underperformed their sunbelt peers during the pandemic. Three apartment REITs with a coastal gateway focus, AVB, EQR, and ESS all reported negative new lease growth rates for Q2 2021. However, performance was significantly better than the previous two quarters. Further, all three reported positive July new lease growth rates, with ESS reporting rental rates for new leases commencing in July increased by 10.9% over the previous expiring lease.

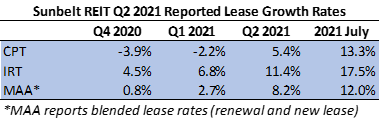

Sunbelt residential REITs CPT, IRT, and MAA have benefitted from pandemic migration patterns and their rental rates have generally outperformed their coastal peers over the past year. All reported positive new lease growth rates for the Q2 2021. Like AVB, EQR, and ESS, new lease pricing was markedly stronger in Q2 compared to Q1 2021 and Q4 2020. Reported July results continued the trend. All three reported rental rates for new leases commencing in July increased by over 10% compared to the comparable expiring lease rate. IRT reported a 17.5% new lease growth for July, with CPT reporting 13.3% for July. MAA reported a blended lease growth rate (new leases rates and renewal lease rates combined) of 12.0%. During the analyst Q&A session, MAA revealed that new lease pricing grew by approximately 17% in July.

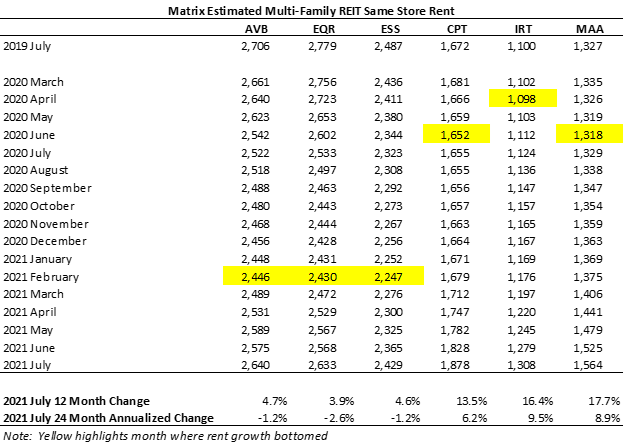

Double digit new lease growth rates are certainly eye catching, but for sunbelt operators asking rental rates bottomed in the spring and summer of 2020, in other words the Q2 2021 and July 2021 comparisons are from a favorable base.

For example, using Matrix rent data to recreate MAA’s same store average rent shows that MAA’s average asking rent plateaued in the late fall and early winter of 2019 and then declined through June 2020 before resuming sequential monthly growth. For sunbelt portfolios, current year over year comparisons are based off a relatively low base. A two-year comparison of MAA’s same store average rent reveals an 8.9% annual increase. Certainly impressive, but not 17.5%.

Conversely, for coastal portfolios Matrix same store rent data suggests new lease pricing did not bottom out until February 2021. Year over year comparisons are still relatively difficult for these portfolios. However, now that these portfolios are also recording sustained sequential monthly asking rent increases, comparisons will get easier in the second half of 2021.

In short, expect continued strong rent performance for sunbelt portfolios, but outsized year over year comparisons will become harder to produce in the second half of 2021. For coastal apartment REIT portfolios, don’t be surprised to see some outsized year over year new lease rental rate comps in the second half of 2021 and possibly continuing into Q1 2022.

Add Comment