The national eviction moratorium put in place last year was designed to prevent poor tenants from being thrown into homelessness during a pandemic. While tenants largely have been kept in place, much of the impact has been felt by mom-and-pop landlords, who don’t have the resources to survive non-paying tenants and have been slow to access federal renter assistance.

The Centers for Disease Control and Prevention (CDC) last week renewed through October 31 its eviction ban in areas hard-hit by COVID-19, putting the national spotlight on evictions just as multifamily fundamentals are hitting unprecedented new highs.

Setting aside legal challenges to the moratorium, the action exposes the bifurcated COVID-19-era economy and real estate market. Larger, professionally managed properties that cater to a more upscale tenant base are performing better than assets and tenants in smaller properties. “It’s a tale of two different worlds,” said a researcher at an industry trade group.

What’s more, the bifurcation exposes vulnerabilities in the rental housing market—such as the need for better aid mechanisms, relaxed limitations on supply and better data in the middle market segment—that must be fixed to solve the nation’s longstanding housing woes.

Eviction Ban Extended

According to studies by Moody’s Analytics and the National Equity Atlas (NEA), 6.4 million renter households are behind on payments. Moody’s estimates that as of mid-year, tenant households owe an average $4,270 in back rent, for a total of $27.5 billion, while the NEA estimates that the average household in arrears owes $3,300, for a total of $21.3 billion.

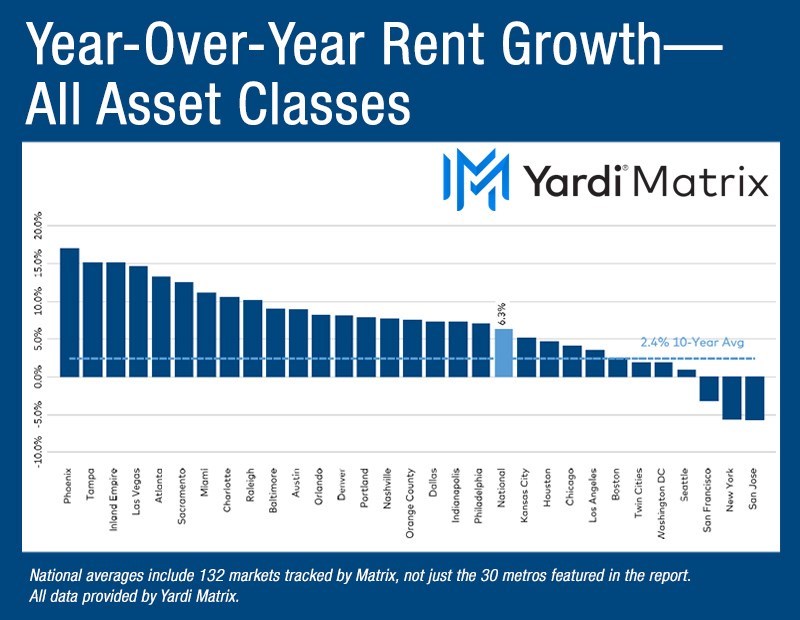

The latest CDC action was a response to pressure from advocates for the poor, who warned that unless the ban was extended, millions of tenants could be evicted and possibly thrown into homelessness. Yet one argument for ending the eviction moratorium is that it has contributed to the eye-popping rise in apartment rents in 2021. Year-to-date through July, multifamily asking rents jumped 8.3%, the largest increase in decades, according to Yardi Matrix data. Year-over-year, asking rents are up more than 10% in nearly half of the top 30 metros, while rents are rebounding rapidly in gateway markets that saw steep drops during the pandemic.

Rent growth is being driven by intense demand. In the 12 months through June, 423,000 multifamily units have been absorbed nationally, according to Matrix, the highest 12-month total in the last two decades. That has pushed U.S. occupancy rates of stabilized properties to 95.3 percent in June, up by 60 basis points year-over-year and close to record-high levels, per Matrix.

Bifurcated Market

All this raises the question: how are multifamily market fundamentals so robust if upwards of 15% of renters are behind on payments? The answer seems tied to the bifurcated nature of the economy. Renters in arrears seem to be concentrated in smaller properties that are not captured by the data derived from professionally managed apartment properties that typically cost more to rent than properties owned by small investors, and whose tenant base is wealthier than the average renter.

Since the start of the pandemic, the National Multifamily Housing Council (NMHC) has published a rent tracker that captures payments of 11.7 million professionally managed apartment units. Rent payments in this survey have consistently been only 1-2 percentage points behind pre-pandemic levels. In 2021, overall payments have ranged between 93.2% in January and 95.9% in March.

The news about smaller properties isn’t as good, however. A survey by the Washington, D.C.-based Urban Institute and Avail.co found that since March 2020, 87-90% of tenants in properties with less than five units have paid rent each month, which is a 500-600 basis point higher rate of non-payment than in professionally managed units. Tenants in properties owned by mom-and-pop investors have, on average, lower incomes, and are more likely to have lost income during the pandemic than tenants at larger properties.

Smaller rental properties are more likely to be owned by mom-and-pop investors and have lower rents than institutionally owned apartments. The difference in ownership size is important in other ways. Studies show that professional apartment managers are generally more aware of, and have the resources and expertise to apply for, the $46 billion of federal renter assistance passed by Congress in 2020 and 2021.

Read the full analysis: Why Multifamily Thrives as Eviction Wave Looms

Add Comment