The average U.S. asking rent continued to decelerate on a year-over-year basis but marks a $3 gain in March.

Report highlights:

- Short-term rent growth picks up following four months of negative growth.

- Renter-by-Necessity rents rose 0.3%, Lifestyle rents rebound, up 0.2% in March.

- Demand remains strong despite economic slowdown.

- SFR rents gained $5 to $2,079, up 2.8% year-over-year.

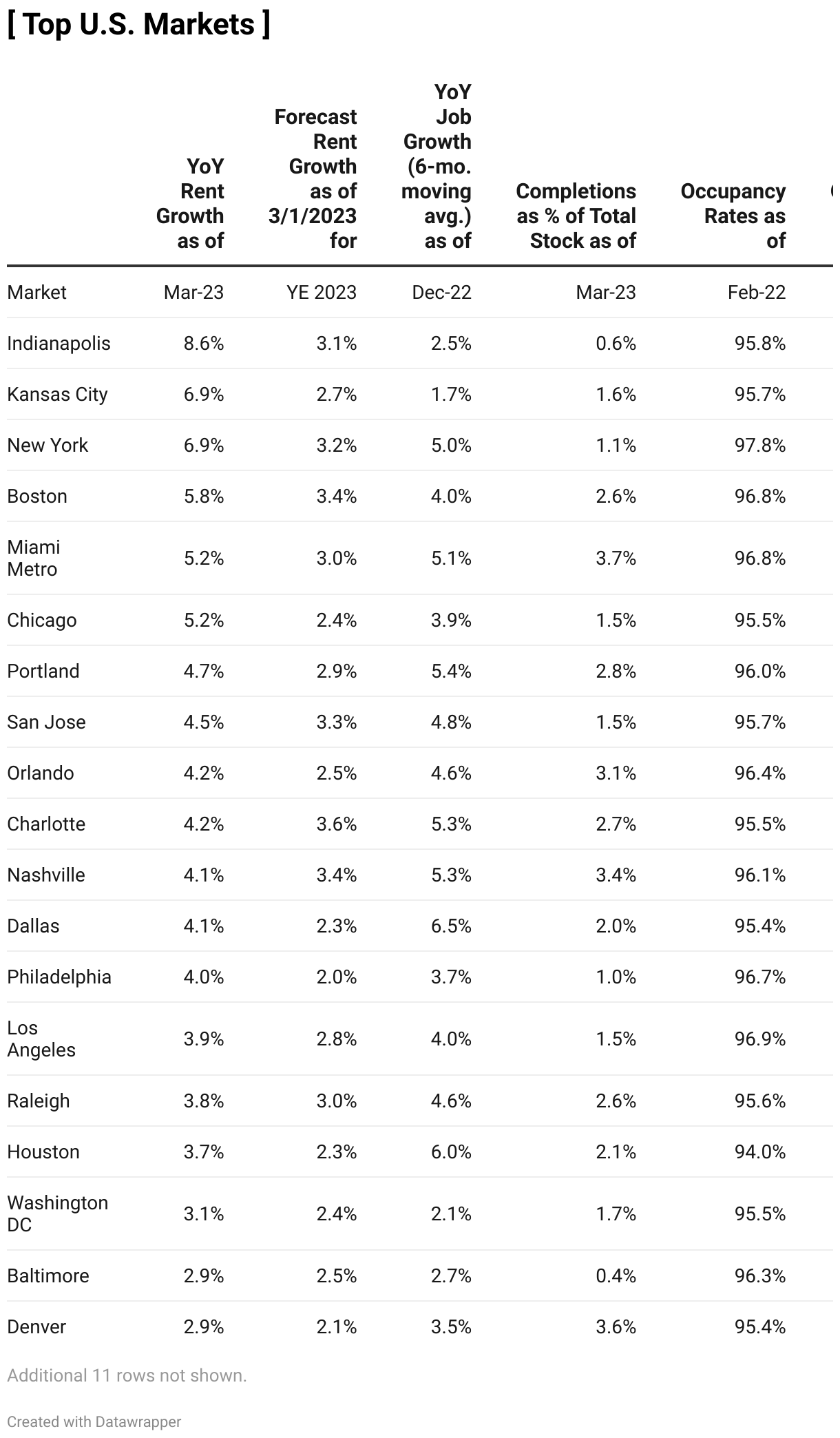

Multifamily rents rose $3 to $1,706 in March, a 4.0% year-over-year appreciation and 90 basis points below the February rate. The rate marks the lowest level since April 2021, when rents began their record performance. The collapse of several banks keeps the financial markets volatile but multifamily property fundamentals remain stable, with rents and occupancy flat during the first quarter of the year. In addition, 21 of Yardi Matrix’s top 30 metros recorded rent gains in March. However, housing affordability issues intensify, which will likely moderate further rent growth.

Midwest and Northeast markets occupied top positions in Yardi Matrix’s top 30 metro rankings, led by Indianapolis (8.6%), New York and Kansas City (6.9%), Boston (5.8%) and Chicago (5.2%). Meanwhile, the occupancy rate slid 10 basis points to 95.1% in February, caused by a decline of the same value in the Renter-by-Necessity segment, which clocked in at 95.2%.

The tight job market paired with high single-family home prices and mortgage rates, and still strong balance sheets continue to boost household formation. Yet, the sharp interest rate increases will likely soften the economy in the second half of the year and moderate demand.

Lifestyle rents rebound, trail RBN

Short-term Lifestyle rent growth went from negative last month to a 0.2% increase nationally, with 19 of the top 30 metros posted increases in March and 10 marking declines. Meanwhile, RBN rents gained 0.3% nationally, with 21 metros registering increases and eight posting decreases. The highest monthly rate increases were led by Acela Corridor metros Boston (1.0%), Washington, D.C. (0.8%), New York (0.6%) and Baltimore (0.5%), and Indianapolis (0.8%).

Renewal rents rebounded, rising 0.3% to 9.3% year-over-year through January. The rate has been decelerating since the 11.0% high last fall and is expected to descent closer to asking rent levels, which stood at 4.0% in March. This burst of growth shows that many renters afford increases, that demand is still strong, and that renters who consider moving to reduce their monthly expenses have limited options in many metros. National lease renewal rates decelerated further, to 64.9% in January, down from 65.2% in December. This steady performance could change as new supply is delivered is absorption turns negative.

Demand strengthens in the Single-Family BTR segment

The SFR segment posted a weak performance throughout the last quarter of 2022, but the asking rent increased 2.8% year-over-year, the equivalent of a $5 gain to $2,079 in March. Occupancy decreased 10 basis points to 95.5% in February, 60 basis points below the February 2022 rate.

The capital climate is challenging to the sector, with some SFR owners announcing layoffs and/or cutbacks in acquisition plans, while the increased cost of construction financing complicating efforts to expand via build-to-rent programs. Still, there are drivers supporting its growth, including tepid single-family home sales due to high mortgage rates and prices.

Read the full Matrix Multifamily National Report-March 2023

Add Comment